A new standard for liquidity in AMM-Based Financial Systems

The first comprehensive, regulator-aligned methodology for sizing and managing liquidity in automated market makers used for CBDCs, tokenised assets, and next-generation settlement networks. Built to solve the critical question the industry has overlooked:

How much liquidity does an AMM-based financial system actually need?

How much liquidity does an AMM-based financial system actually need?

Understand the Breakthrough Behind

The Jackson Liquidity Framework

A clear and accessible explanation of the liquidity dynamics, mathematical models, and findings inside the whitepaper — designed for everyone from crypto beginners to central bank researchers.

The Jackson Liquidity Framework was created to answer the biggest unanswered question in tokenised finance and CBDC settlement:

How much liquidity does an AMM-based financial system actually require?

How much liquidity does an AMM-based financial system actually require?

The Problem No One Had Solved

Why AMM Liquidity Is a Missing Piece in Modern Banking

The future of money is moving toward:

- Tokenised assets

- CBDCs

- Instant cross-border settlement

- Automated FX conversion

- Pre-funded liquidity pools

But unlike traditional RTGS systems, AMMs introduce non-linear liquidity requirements that change with flow patterns, volatility, and directional imbalance.

Yet — until now — no regulator, bank, or academic body has produced a formal liquidity sizing framework for AMM settlement.

The Jackson Liquidity Framework fills this gap.

The future of money is moving toward:

- Tokenised assets

- CBDCs

- Instant cross-border settlement

- Automated FX conversion

- Pre-funded liquidity pools

But unlike traditional RTGS systems, AMMs introduce non-linear liquidity requirements that change with flow patterns, volatility, and directional imbalance.

Yet — until now — no regulator, bank, or academic body has produced a formal liquidity sizing framework for AMM settlement.

The Jackson Liquidity Framework fills this gap.

The Core Dynamics Behind AMM Liquidity

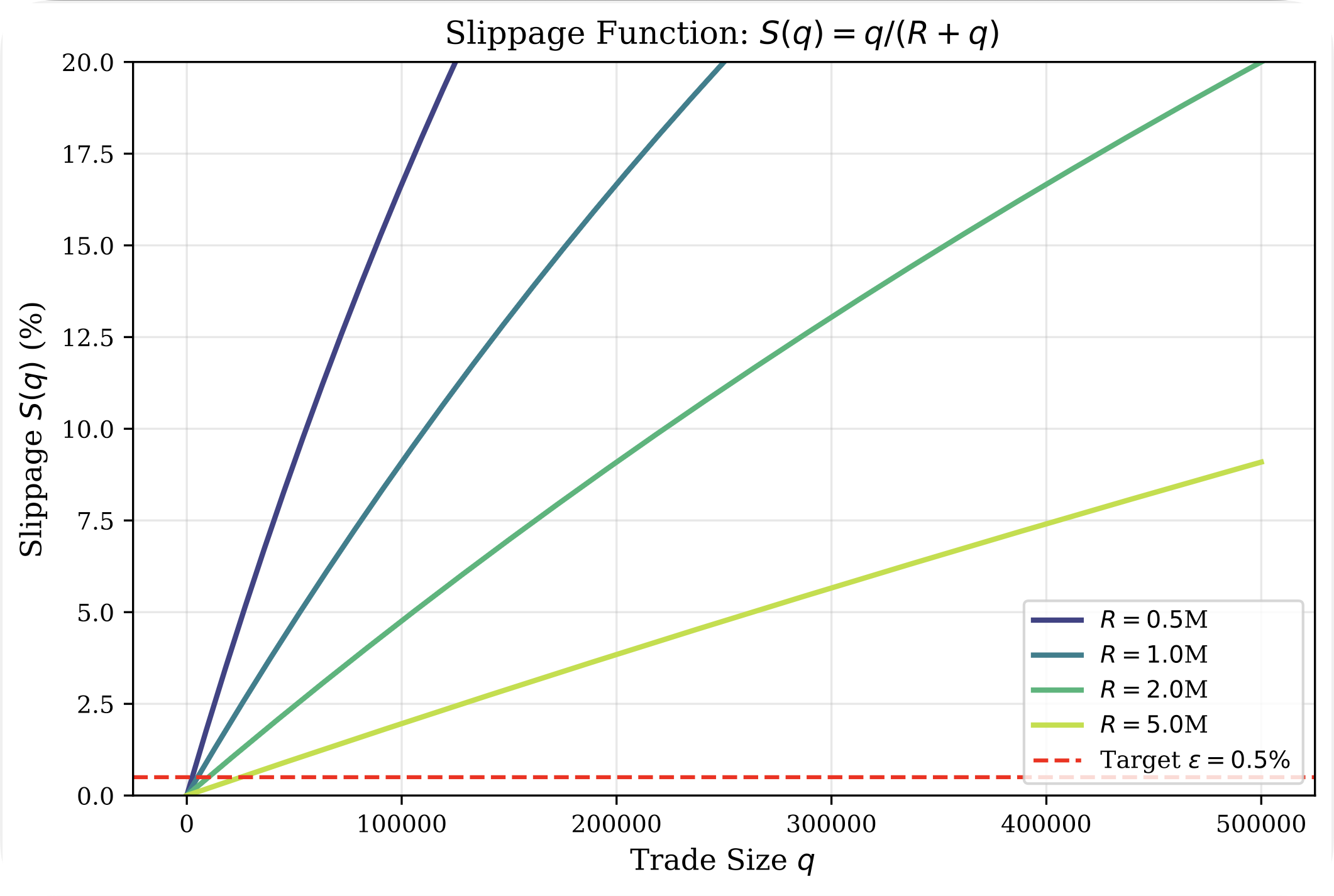

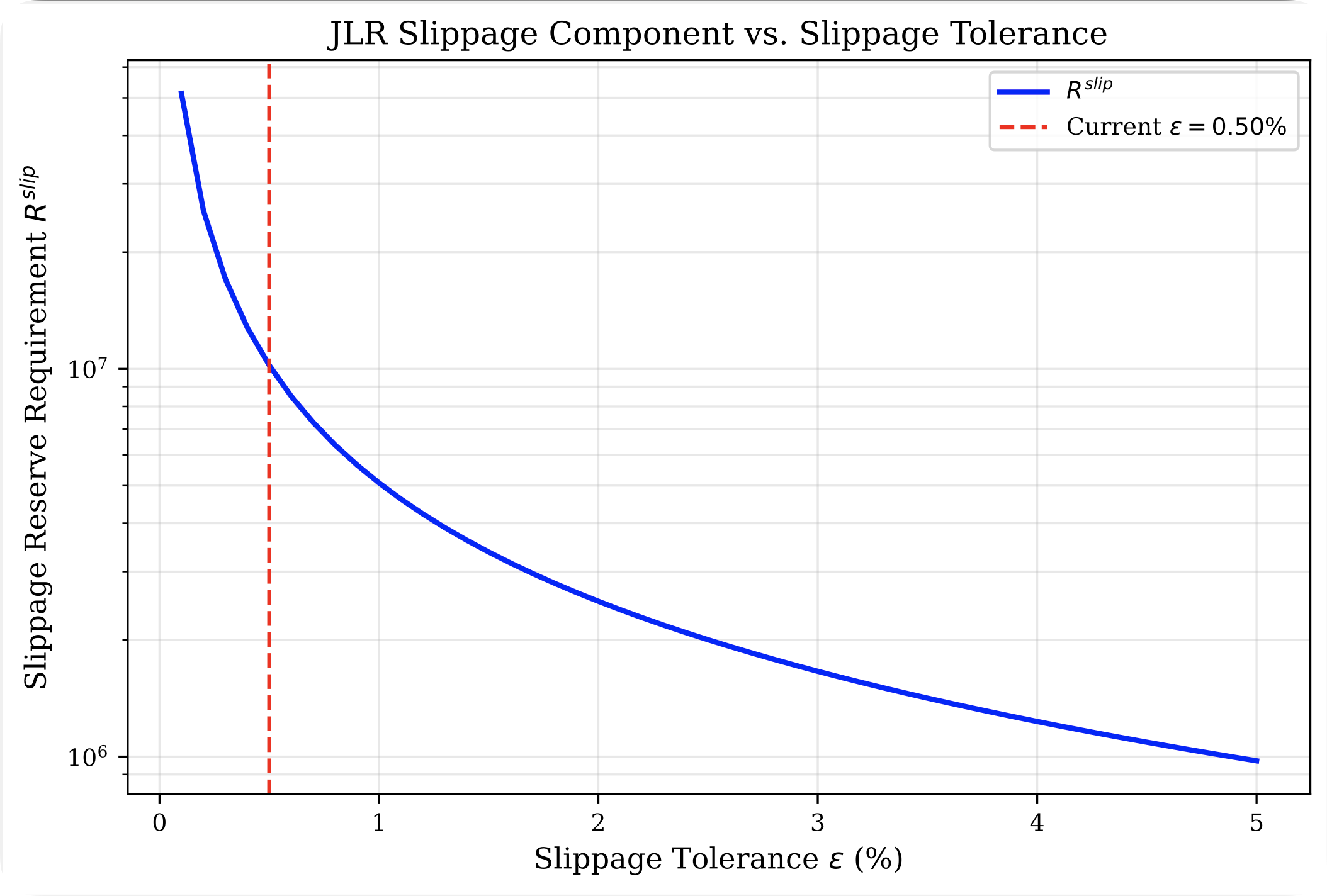

1. Slippage (The “Shallow Pond” Effect)

- When liquidity is shallow, even small trades cause large price impact.

- When liquidity is deep, impact is minimal.

- This makes AMM liquidity non-linear and dangerous when reserves are low.

- When liquidity is shallow, even small trades cause large price impact.

- When liquidity is deep, impact is minimal.

- This makes AMM liquidity non-linear and dangerous when reserves are low.

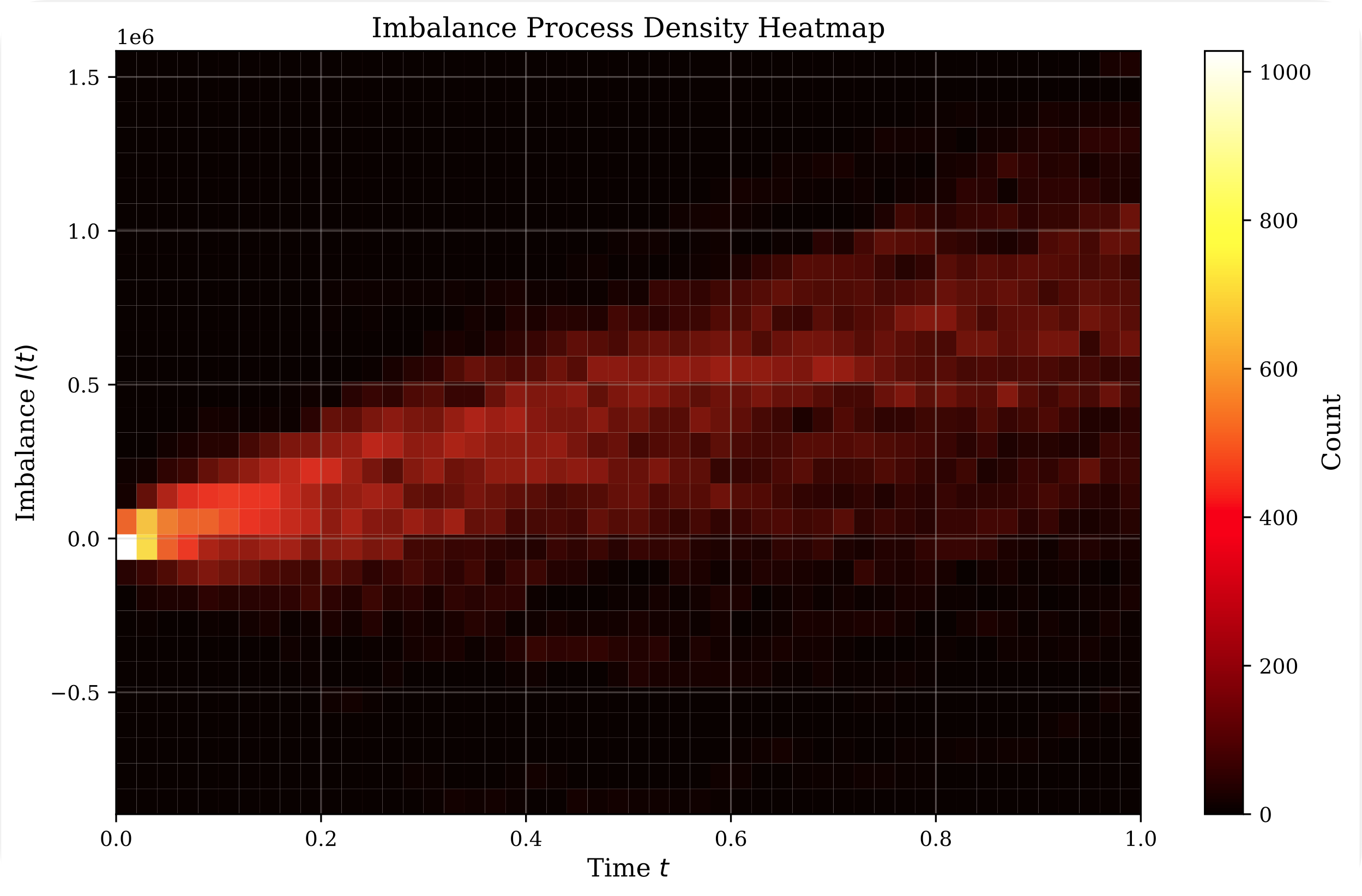

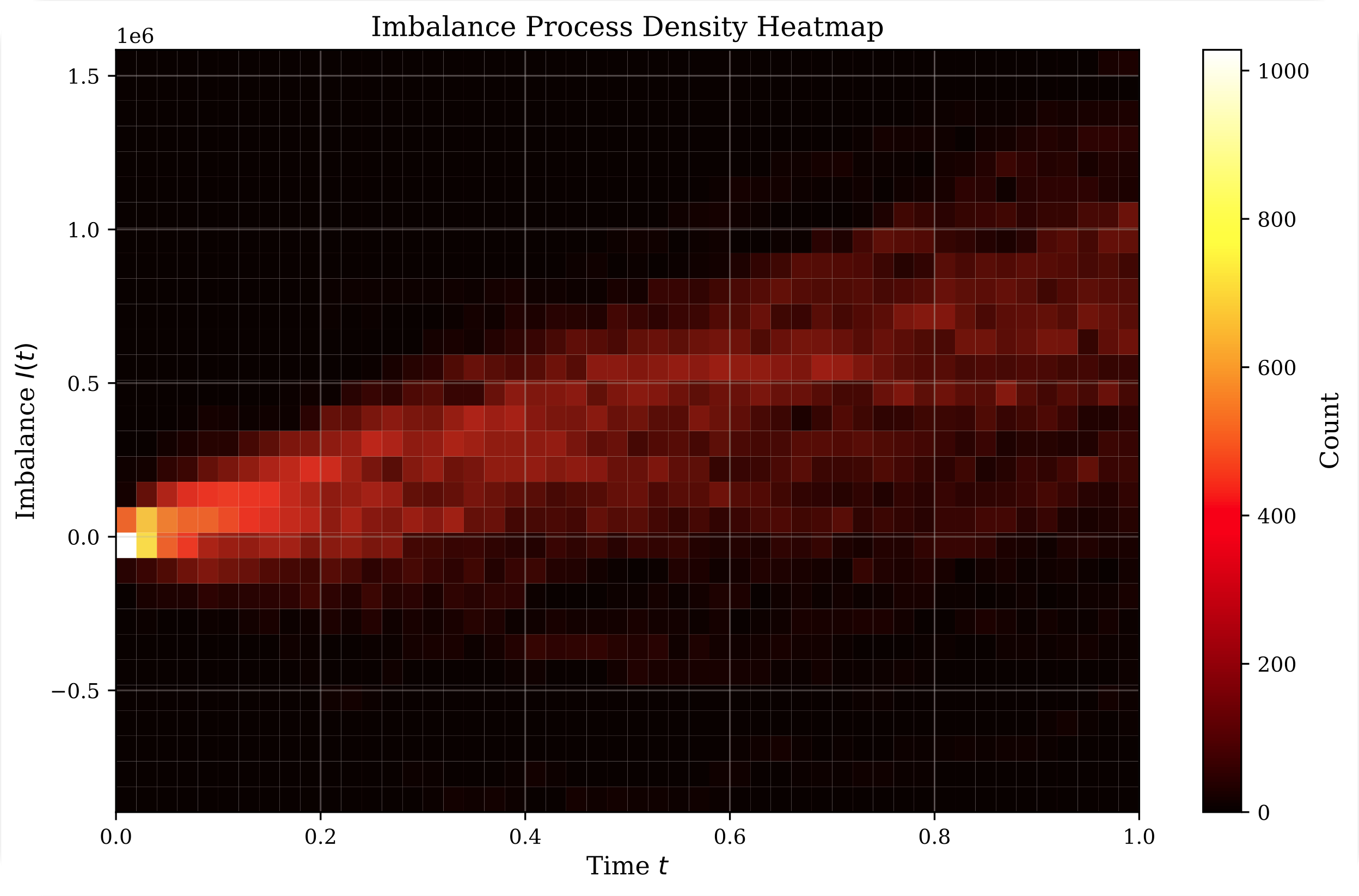

2. Directional Flow Imbalance (The “Seesaw” Effect)

Real payment corridors rarely balance perfectly.

If more flow moves in one direction, AMM reserves drain — quickly.

Real payment corridors rarely balance perfectly.

If more flow moves in one direction, AMM reserves drain — quickly.

3. Intraday Clustering (The “Storm” Effect)

Payments don’t arrive evenly. They arrive in clusters, especially around cut-off times or liquidity cycles.

Clustering can multiply liquidity demand by 2–4×.

Payments don’t arrive evenly. They arrive in clusters, especially around cut-off times or liquidity cycles.

Clustering can multiply liquidity demand by 2–4×.

Introducing the Four Jackson Components

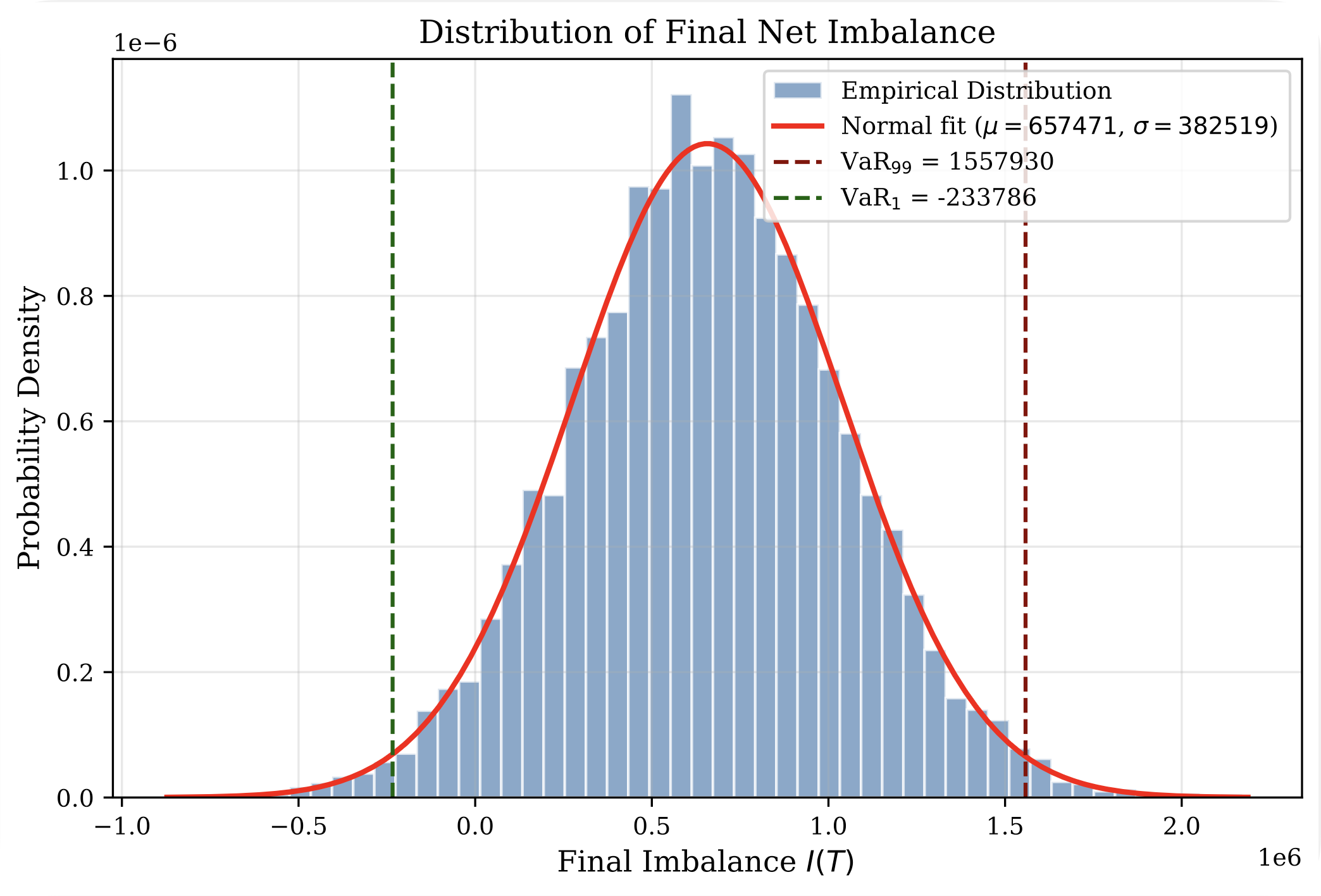

JLR — Jackson Liquidity Requirement

Defines the minimum reserve depth required for safe AMM settlement.

Combines four factors:

- Slippage

- Directional flow VaR

- Intraday liquidity peaks

- Basel III constraints

Defines the minimum reserve depth required for safe AMM settlement.

Combines four factors:

- Slippage

- Directional flow VaR

- Intraday liquidity peaks

- Basel III constraints

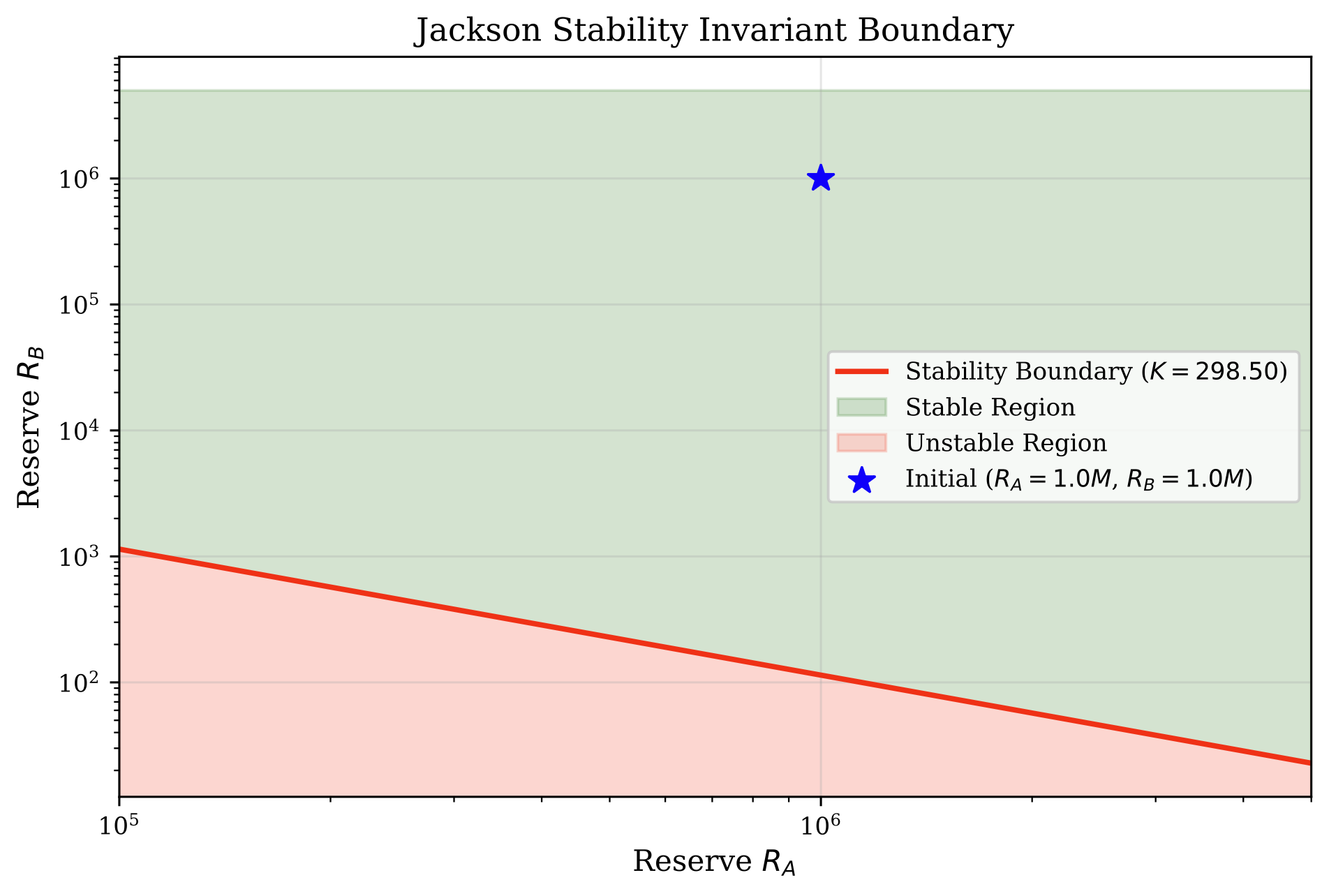

JSI — Jackson Stability Invariant

A solvency-style boundary showing when a pool becomes unstable.

If reserves fall below this curve, the AMM becomes fragile.

A solvency-style boundary showing when a pool becomes unstable.

If reserves fall below this curve, the AMM becomes fragile.

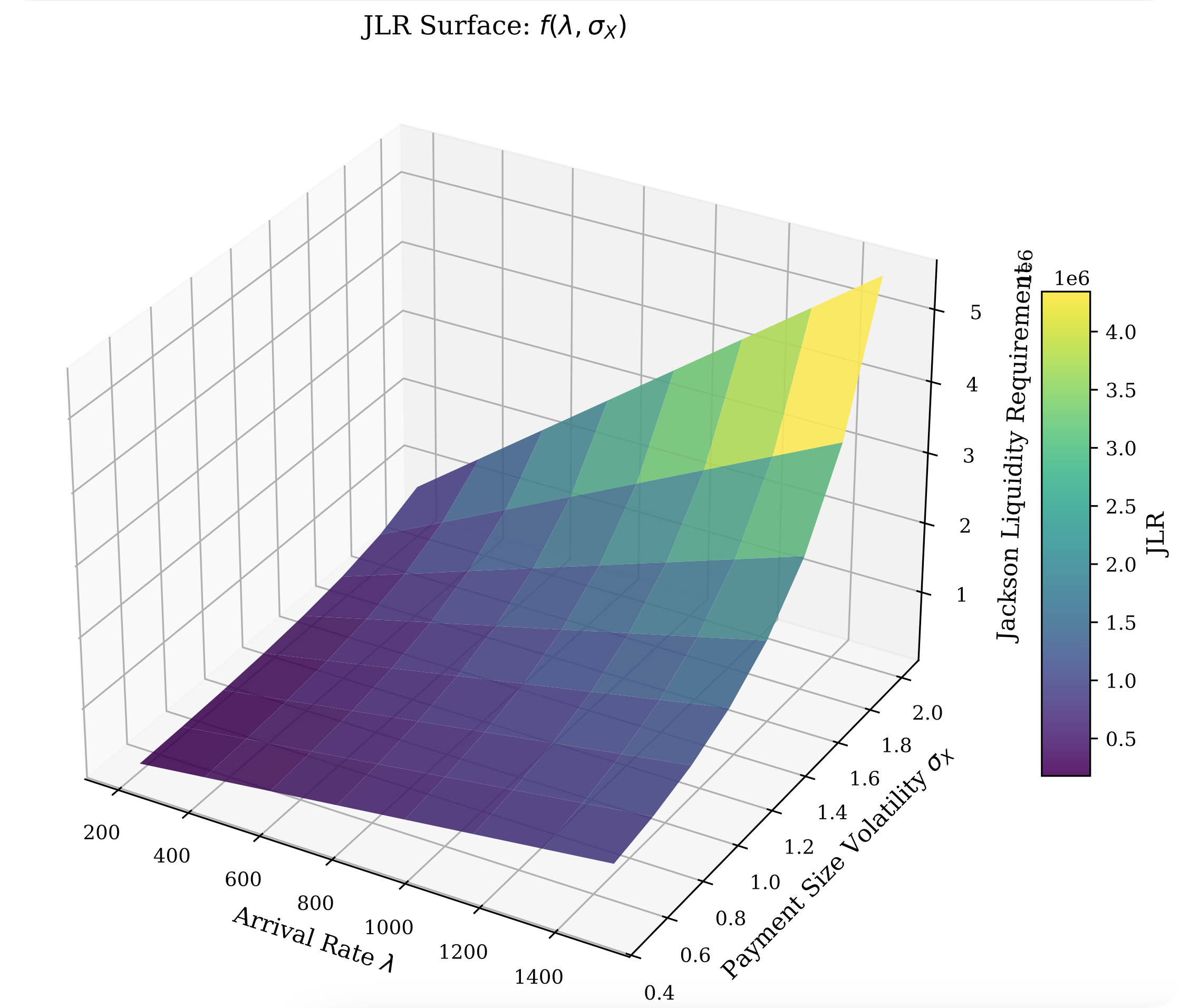

JLS — Jackson Liquidity Surface

A 3D map showing how liquidity demand rises with:

- Arrival rate

- Payment size volatility

- Corridor conditions

A 3D map showing how liquidity demand rises with:

- Arrival rate

- Payment size volatility

- Corridor conditions

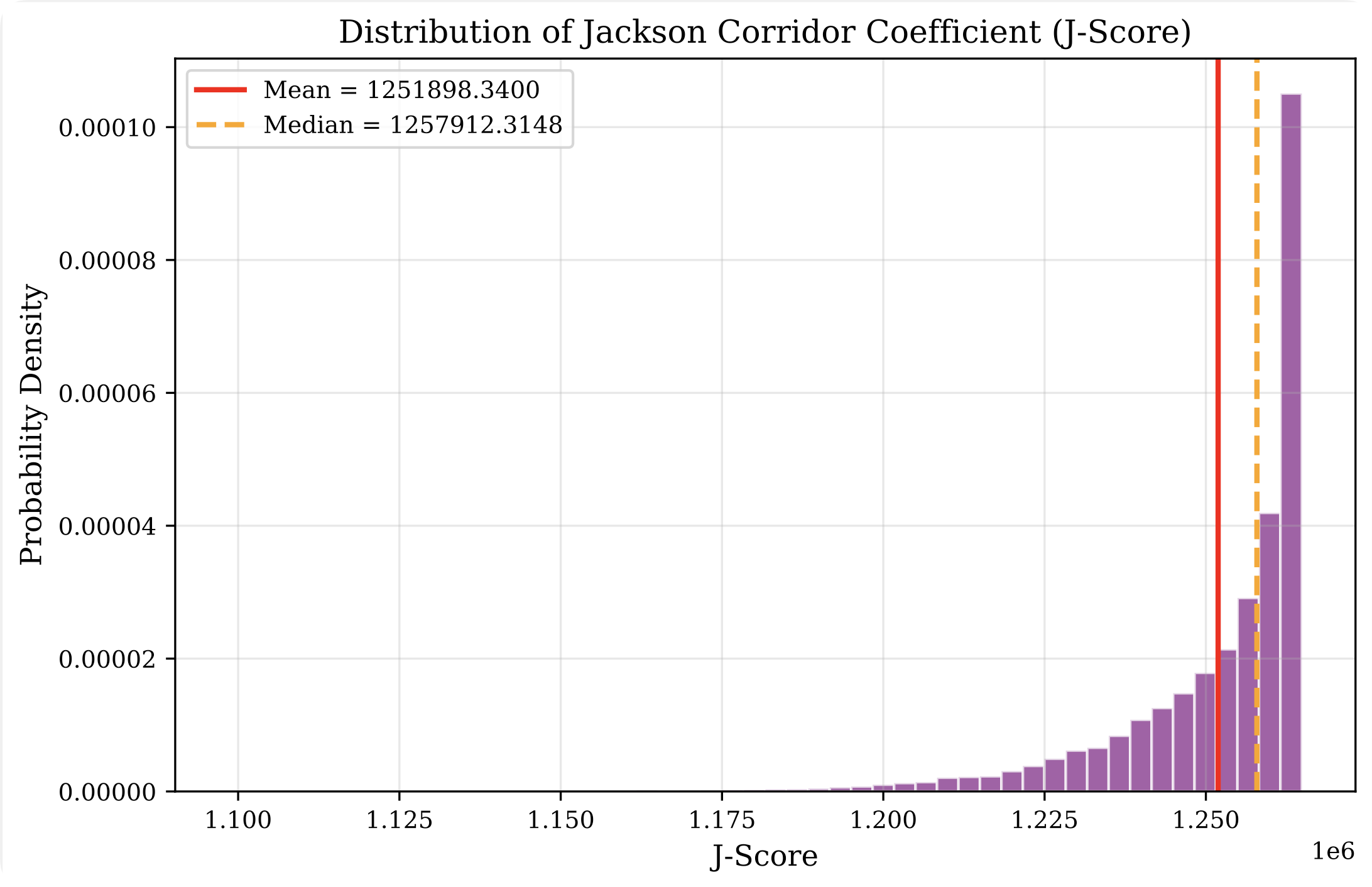

J-Score - Jackson Corridor Stress Metric

A single number that expresses settlement stress — instantly.

Used for monitoring and real-time decision-making.

A single number that expresses settlement stress — instantly.

Used for monitoring and real-time decision-making.

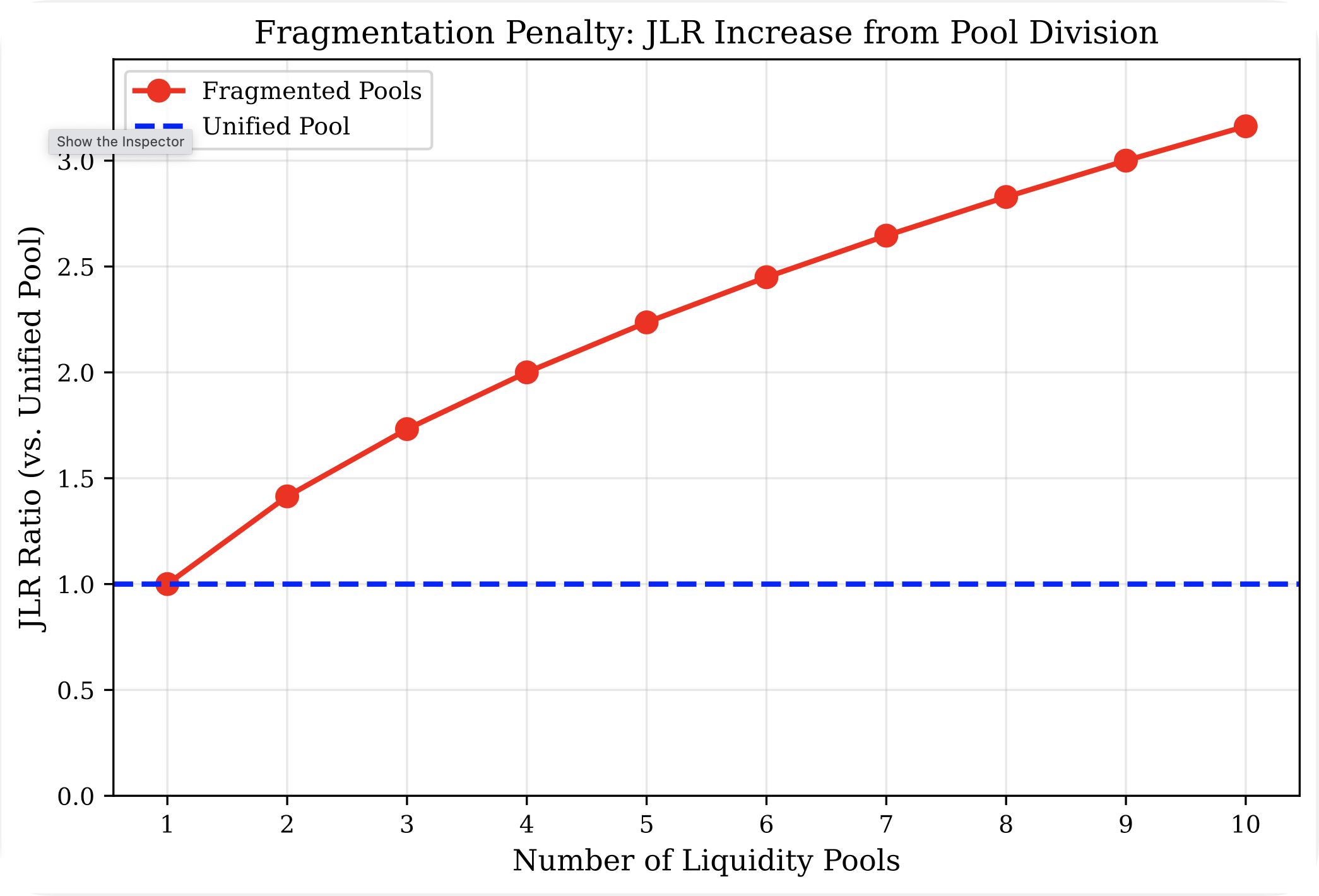

Fragmentation: The Hidden Liquidity Killer

Splitting liquidity across multiple pools dramatically increases the total amount needed — sometimes by 900%.

A single unified pool is always more efficient than many shallow ones.

A single unified pool is always more efficient than many shallow ones.

What This Means for CBDCs, FMIs, and Banks

The Jackson Liquidity Framework brings mathematical clarity to a problem regulators have acknowledged but not defined.

By integrating slippage constraints, stochastic flow models, and intraday liquidity peaks, the framework creates a liquidity model suitable for real-world CBDC settlement networks.

By integrating slippage constraints, stochastic flow models, and intraday liquidity peaks, the framework creates a liquidity model suitable for real-world CBDC settlement networks.

Try the Tools That Power the Research

See the framework come alive through my interactive simulator.

Experiment with:

- Poisson vs Hawkes flows

- Real-time slippage curves

- Reserve depletion paths

- J-score monitoring

- Fragmentation penalty modelling

- The full JLS Surface

Experiment with:

- Poisson vs Hawkes flows

- Real-time slippage curves

- Reserve depletion paths

- J-score monitoring

- Fragmentation penalty modelling

- The full JLS Surface